Pitch It!

Presentation design book

Pitch It!

Presentation design book

This book touches on all aspects of presentation design: layout, colours, fonts, story telling, tools, data visualisation, and discusses the dynamics of investor and sales presentations.

Click one of the thumbnails to read a chapter, or pick a chapter from the "book" drop down menu at the top right corner of this page.

You can also install this book as an iBook on your iPad (free). Click here to go to the app store

1 - Introduction

It takes both skill and courage to design presentations

1 - Introduction

It takes both skill and courage to design presentations

You do not like sitting through presentations, neither does your audience

People are natural born story-hearers. Huddled around campfires or across dinner tables, hearts and ears opened as messages were orally passed down from one generation to another. It was the storyteller’s craft to spin the story well. By skillfully weaving a resonating plot, audiences were engaged and inspired for centuries, without the help of technology.

These past 30 years have ushered in unprecedented communication technology: slide design software, video, audio. Yet, as we progressed, these innovations seemed to have pulled us away from well-crafted stories. This is especially apparent in business, where "death by PowerPoint" hits presentation audiences and leaves them devoid of any memorable experience.

The goal of this book is to reverse this phenomenon, and retrieve the spark of stories now to be handed down through slideshows that leave a mark on listeners. By fast-forwarding you through a process that took me half a decade to complete, you’ll become a skilled crafter of great presentations.

Starting as a computer science engineer, then moving on to strategy consulting with McKinsey & Company, I’ve reinvented myself as a creative professional. Now I design presentations for a living. I will share with you important insights gained through this transition, and let you in on the secrets that make presentations enjoyable and effective.

This books is not oriented at a specific software tool, to serve you as a manual would. Rather, you can apply the skill offered here to any program you use to create your presentation. Even better, this book ensures your audiences will wonder what software you used, evoking questions such as “Can PowerPoint create presentations like this?” A real compliment to any presentation designer.

Three common mistakes can be avoided

We’ll tackle three common habits that immediately give you away as an amateur presentation designer:

- Amateurish slide design: poor choice of fonts, colors, and layouts. A few very basic design suggestions will have a great impact on how your slides look.

- PowerPoint takes control: the software you used dictated the way you wrote your story. Technology should not hinder storytelling, only enhance it.

- Blah, blah, blah: under the slightest stress of speaking in public, and we all tend to switch to a more formal language.

Audiences are best engaged when spoken to directly and articulately.

The good news is that these faults can easily be overcome. Together, we’ll improve your technical skill and discuss simple tips and tricks that dramatically impact any presentation.

But, most of all, I want to give you courage, and empower you to deviate from the common practices of presentation design. Your way of presenting things differently is not crazy, and people will not laugh at you. Originality and candidness are excellent yarn for knitting ideas together well, and conveying a lasting message.

While this book is written with sales and investor presentations in mind, its concepts are applicable for a broad range of slideshows. Whether you work in a two-person startup or a large multinational corporation, anyone can benefit from its contents. Great presentations leave your audiences elated and with a taste for more of what you have to offer. It is a memorable experience, to which this book offers key ingredients.

Nobody has ever blamed a presenter for finishing early. To reflect this, I’ve kept content short and very much to the point throughout the book. Instead of spending lots of time and pages on convincing you why certain presentation styles are bad, I focus on tangible and practical suggestions to make your presentations better.

Links to products in Amazon or iTunes that appear in this book are affiliate links, with retailers granting me a commission for purchases made from the book. This does not affect the price that you are charged for the products.

I hope you’ll find this book insightful, empowering you with the skill and courage you need to create great presentations. Everyone loves a good story, where information unfolds in a motivating and inspiring way. So share the message across, and reignite the essence of storytelling in the great presentations you’ll make from now on.

Tel Aviv, December 2012

2 - Visual slides

An alternative for bullet points in presentations

2 - Visual slides

An alternative for bullet points in presentations

Bullet points are slide killers

BULLETS ARE BORING

Bullet points don’t do well for staging your message professionally. As I see it, Microsoft is not to be blamed, because PowerPoint itself is just a software, not a method. It’s the way people use it that has oddly inflicted a whole generation.

A good example for this is PowerPoint’s default slide template. This opens up on any new presentation, displaying a host of bullet points on a blank slide just waiting to be filled. But look at the text below:

- By the time I have finished

- reading out these bullets to you,

- you could have read them yourself

- 3 times over, while also replying to a

- bunch of emails on your mobile.

Your audience reads bullets much faster on their own, without you. Once they realize that in the next 30 minutes all you’ll be doing is reading out magnified bullet points from slides, they’ll invest their attention elsewhere.

Bullet points are good practice for jotting down thoughts, sketching a rough storyline and listing talking points for yourself. They could be the starting point, but are definitely not the end point of your presentation design effort.

Get rid of bullet points by sticking to one-idea-per-slide

THE RIGHT ALTERNATIVE

There is a better and very simple way to design a presentation without giving in to our tendency to fill up pages with bullet points: stick to one idea per slide. This is good practice because, at any given moment, audiences focus only on one idea delivered in the storyline.

Yes, the one-idea-per-slide rule of thumb may dramatically increase the number of slides in your presentation. And this could go against common restrictions that limit the presentation time by sticking within page count constraints, logic being “fewer slides, fewer minutes.” But often, less slides entail even more content, tightly crammed over each page with free space used up for text and bullet points. The slide count restriction makes people design very dense slides that still take a long time to present.

Ignore page count restrictions, but stick to your time limit

My advice is to ignore the page count restriction, but stick to the time constraints that you were given. A presentation with many slides can be given in exactly the same amount of time as one delivered with a few slides that are loaded with bullet points. This is because you simply go through the slides faster, while your audience is kept focused.

Why are bullet points so persistent? One reason is the habit instilled by the default PowerPoint template. Another reason could be plain laziness, since it’s become quite the norm to relate to a few bulleted pages as a finished slide deck. And there are also historical reasons.

Back in the 1980s and 1990s, presenters used overhead projectors to stage their ideas, uncovering parts of transparent slides along a storyline. Later, with the arrival of word processors, transparent slides showcased whole printouts of freshly authored documents, sometimes page by page, bullet by bullet.

Slides and presenter are to play in unison, forming together a complete visual experience - literally a Slide Show. Slides are intended to support the storyline narrated by the presenter, with a continuous stream of visuals in the background. Work on gaining that total picture, and appealing to the audience as a clip or video would, where you/presenter narrate the plot that is visualized on your slides.

Moreover, you are responsible of orchestrating the Show of Slides. The conductor’s baton for this, is the remote control you’ll hold in your hands to rapidly scan through the slides. Otherwise, you’ll be glued to your computer, pressing the page-down button away every 30 seconds to streamline the flow of slides. With a small remote control in your hand, you’re better off changing slides without the audience even noticing your timely shuffling. And you can keep direct eye contact with the audience, engaged at all times.

LITTLE TEXT, LOTS OF PICS

Another argument against bullet points, is the fact that text is an incredibly inefficient way to transfer information. This is especially apparent in content that lacks actual visual meaning. This is because the brain has to read the words, assemble sentences and only then visually phrase its meaning. The ability to convey a message quickly grasped by the brain in mental pictures, is key in any good presentation.

A food critic sits in a chic restaurant in Paris, alone at a table behind a good bottle of Bordeaux. He takes the first bite of his ratatouille, and - O! He experiences a flashback to his childhood in Provence, where his beloved mother prepared this very same dish he savored after a tedious day at school. Boy, did this taste good

This text fragment is taken from the Disney/Pixar Ratatouille movie scene. I included a screenshot of the movie. Compare the picture to the text, and, as the old saying goes “A picture is worth a thousand words,” because a simple image describes scenes better. You get it in a second. Images have a much higher data transfer rate, not only in terms of bits/cm². But there is more.

Images are emotional pieces of information

IMAGERY FOR MEMORY

Images are emotional pieces of information. Emotion plays a big part in memory, triggering a recall of information, similar to the food critic taking a bite and unlocking a rich set of childhood memories (visuals, smell, sounds).

Advertisers use this technique all the time. Powerful images displayed on billboards, printed media, TV commercials, all hammer branded messages into our brains. Remember the Benetton ads from a few decades ago? Some advertisers push this technique of emotional shock to the extreme.

You have access to the same image databases as professional designers

The objective of your presentation is pretty much the same, so find the right visual to appeal to your audience’s palate, and make your story memorable.

An example. Pitching to investors a new company that developed technology for more sticky websites, if you were to use bullet points, you’ll probably boast the slogan “We make websites more sticky.” Everyone will read this, and most probably forget it a bit after the presentation. If you include an image, say a threatening one of a user zapping away on their remote, chances are these investors will remember the slide and message even after 3 months.

There are other good presentation props that have strong emotional stimulus, besides visuals. This is where your originality and creativity can really boost the show. In a recent TED talk, Bill Gates wanted to give the audience a feel of what it’s like to live within range of malaria mosquitos all the time. He release a few mosquitos into the audience (watch the video here). I am sure the people sitting in the room got the point. Moreover, they will not forget it. Nancy Duarte in her book Resonate refers to this as a STAR: Something They will Always Remember.

Pictures are not always the right solution

EXCEPTIONS

Not all the slides in your presentation or, in fact, all presentations, are suitable for the big picture, big font, little words style. Here are some exceptions.

- A graph or a table illustrating a batch of data obviously needs to contain more information. We’ll discuss designing good data charts later in this book.

- When the whole point of your slide is to emphasize the relationship between a number of things, there is no alternative than mentioning them all on one slide. Stretching the message across several individual slides may loosen their relativity. In such cases, find a creative solution and avoid listing them as bullets. For example, you can use brief explanations in interconnected text boxes to illustrate the relationship.

- Keep in mind that an audience of 5 people in a small conference room ready to go over the financial results of last quarter, are more apt to handle denser slides than the large audience of a TED talk.

- In some cases you might use PowerPoint or Keynote as a word processor to write a document that is meant for reading, not for presenting. That is perfectly fine.

It is completely okay to mix styles within one presentation deck. Often, you’ll need to use big bold visuals in the opening sequence of your presentation, just to make a grabbing statement about the problem the company you are pitching is about to solve. Later on in the same presentation, you can switch to a denser slide design, for example, when you discuss the financials, list competitors, or point out the company’s strategy.

Some people take the idea of “one idea, one picture” too far. I’ve seen presentations were every single word was supported by some sort of image, regrettably even cliché ones. For example,

- We are under pressure (visual of orange press) [click]

- and the company is entering a slippery slope (visual of a ski piste) [click]

- as we are thinking hard (visual of confused man) [click]

- about a possible way forward (visual of an open road ahead).

This type of slide design is popular on online slide sharing platforms, such as SlideShare. Maybe it works for an online audience, but for a live audience, 10 clicks per minute shuffle too many slides, too many random images, and too much inconsistency.

In fact, sometimes it can actually work better not to present a slide at all. A blank screen focuses the audience’s attention back to the presenter. In PowerPoint you can create a blank screen or a white screen by pressing “B” or “W” on your keyboard in presentation mode. Personally, I prefer to place an empty slide inside my presentation where needed, to avoid the old slide from popping up again when I press B or W to continue the slide show.

QUICK SUM UP

Keep in mind the distinction between slides that are meant for reading and those meant to support what you are orally presenting. Avoid bullet points. Instead, design visual slides that convey your message across associatively. Don’t be afraid to use images and other emotional props. In the next chapter you will find out where to get good images, and how you should format them.

3 - Images

Finding and formatting images for your presentations

3 - Images

Finding and formatting images for your presentations

Hopefully, you’re now convinced visual slides are far better practice than dense bullet point slides. Our next question is where to get good images for your presentation?

CLIPART, YES OR NO

Clipart was very popular back in the ‘90s, for early versions of Microsoft PowerPoint. Everyone remembers Screen Bean® who bobbed along many presentations across the globe. You can still download this guy from the Microsoft Clipart site.

In 99% of cases, clip art does not work

You should keep in mind, though, that Clipart graphic simplicity renders your slides the look and feel of an invitation to a children’s birthday party, or a neighbor’s garage sale. It is possible to use Clipart sensibly, but it requires much work and dedicated search.

Creating more professional looking presentations using Clipart, requires delving deep into the Microsoft Clipart database, where advanced users can find a set of images that do not have that children’s birthday party look. There are some treasures there to be dug out, like ‘50s style cartoons or pop art characters. Style 802 is a good example. The good thing about clip art is that once you have found a suitable style, there are likely to be many, many, variations based on the same theme, an effect that is hard to achieve with photographs.

After importing the Clipart characters, some editing is required. This could include ungrouping the objects to deleting bits you don’t want, such as unnecessary background graphics. The remaining image can give a very distinct appeal to a presentation, especially if you position it well and scale it up to a grand size, instead of a marginal size icon floating on the page.

GOOGLE IMAGE SEARCH

A major resource many people turn to for presentation images is Google Images. Simply type in a keyword, and millions of images are filtered out for your choice. To improve your selection, Google Images offers additional filtering options, by image size or color. You can even drag an existing image into the search box to return similar findings for you.

However, there are two big drawbacks to Google Images you must keep in mind. First, most of the images are copyright protected, and second, most of the images are of poor quality.

Google Images is excellent for brainstorming on finding the best supporting image for each of your slides. Once you establish a good idea of what you need, turn to stock image sites to find such imagery that is legal to use and comes in high res quality.

STOCK IMAGE SITES

Professional designers buy pictures from image databases to be used in all their projects (ads, brochures, web sites, magazines, newspapers, billboards). These resources are available to everyone, and your presentation can benefit as well from the excellent imagery offered on stock.

Head over to stock image sites such as iStockPhoto or shutterstock where you can search for images by keyword, size, color, and many more search criteria filters. All the photographers on these sites are screened to ensure their high technical quality.

As for usage rights, pictures you buy on these sites allow you full use, as defined on these sites’ license agreements. For presentations, images usually fall in the lowest cost license option, since audience number is far smaller than that of a printed magazine, newspaper or television show.

You can easily download a sample version of the image, sealed with a watermark, and work with it while editing your presentation. Once your presentation is ready, and you are sure of your pick, buy the images and incorporate them permanently or at high res.

Many stock images are over-used and not real

While the technical image quality of stock photo sites is high, the actual visual composition might not always be optimal. Many images are staged, snapped in unnatural environments. For example, it’s pretty apparent the call rep operator is, in fact, a model earning her living posing on photo shoots, and not by courteously answering customers on support calls. The handshake in front of a skyscraper has been used all over the place, so that such a photograph is now just an empty cliché.

To answer the need, some stock photographers go as far as manipulating readymade visuals, creating compositions intended to capture a specific concept presentation designers may seek. They combine images, add illustrations or text. Most overstep themselves as they try to do the presentation designer’s work. Don’t fall for this - make your own compositions. The challenge is to find real, naturally rendered images, which best do the work for you.

A useful search term in stock image sites is “isolated.” It will return images of isolated objects over a white background. You can then easily remove the white background in Photoshop or PowerPoint, making it transparent and allowing you to fit the object well together with other elements on the slide.

Another big advantage of stock image sites is that they allow you to be consistent in the style of images you choose. Often stock photographers produce different images featuring the same model, or follow a uniform visual concept. You can buy 5-10 such images of the same visual language, and design your entire presentation around them. You’ll attain a good consistent look and feel. In this book for example, I went for impressionist paintings.

The same picture can often be found on different sites, and prices can differ dramatically

In terms of pricing, stock photos can vary greatly. Size or resolution make a big difference to the buck. At the time of writing (December 2012) the highest resolution monitor out there is approximately 2,500 pixels wide. While this is great for billboards, most conference room overhead projectors have resolutions below 1,000 pixels wide. Still, it is good practice to download images in their highest resolution possible, to allow you to maintain focus if you zoom in on a specific part of it, or expand it onto a full page.

Often times, stock image sites price images differently. A handy tool for comparing prices across stock images sites is SpiderPic. Enter the image name or URL you want, and this software accesses multiple stock image sites, filtering up the same image with compared prices.

PHOTO SHARING SITES

Photo sharing sites such as Flickr or Instagram have the exact opposite problem than posed by stock image sites. None of the images are staged, but naturally captured, and depict people in real life situations. Keep this in mind as you think of the emotional impact an image may have in your slide.

Photo by Alexander Kess on Flickr

Flickr hosts some great presentation images

On these sites, the technical quality of images varies highly. People posting images to Flickr range from the world’s most famous professional photographers to the world’s worst amateurs. Your challenge is to find the good quality ones that will serve you best.

Keyword searches are less powerful here, in comparison with stock image sites. This is due to the fact, that pictures are labeled for searching by the photographers that uploaded them, and may not be accurate enough to filter in with your keyword search. Color based search is usually not an option. Date search is available on Flickr, a site that, over the years, has accumulated a huge library, inclusive also of older images that you can use to give your presentation a retro feel.

Keep in mind that such public photo sharing sites entail some copyright issues. I advise you to make sure the image you want is licensed under a Creative Commons license. This means you can use the image if you include a credit made to the photographer’s name. You can easily create such photo credits in very small print at the very bottom of your slide. Instagram images are all licensed to the photographers, so you’ll need to contact them for usage permission.

Personally, for my presentation, I have found photo sharing sites a great source of very realistic images, including people, crowds and specific locations.

WIKIPEDIA

WikiPedia is a good alternative source of images without copy right issues. License fees rise highly and are especially an issue if you require images of celebrities or historical news photographs. You can get them, though, from high end image sites such as Getty Images.

The same health warning as Flickr applies for WikiPedia too, stating images are typically not taken by professional photographers. While it is okay to use an image of a celebrity as an example, you’ll find it impossible to base an entire look and feel of a whole presentation, or its branding guideline, without owning permission rights.

GOOGLE EARTH AND STREETVIEW

Google Earth can produce spectacular mapping images for presentations. I find the detailed closeups great, and have often used a tilted map to simulate a pilot’s cockpit view.

Here too, you must watch out for copyright requirements. A professional license of some $400 a year, may be binding for usage right to images in your slideshow.

Google Streetview is a potentially useful source of images, however copyright requirements are even stricter than Google Earth. Google lets you use images only if you link to them via the approved API. This gives Google the option to adjust its images with updates (due to a privacy complaint, for example).

A good approach is to design your draft presentation using Google Streetview imagery. Then, as you are about to complete the final draft, send someone to take the actual shots in the field, and include them in your final version of the presentation.

CRAYONS AND INK

Instead of seeking an answer on the outside, you could go back in time yourself, and create an entire presentation using hand drawn sketches. These little artistic masterpieces can easily be scanned and incorporated well in any PowerPoint or Keynote slideshow.

You’ll find many iPad applications to easily make good hand drawn pictures. Pen strokes come out beautifully, even better than ink on paper, some would say. It’s also easier to correct and erase any part of an existing illustration at any time. These tablet drawing apps are really good for creating natural looking handwriting, you can deliberately enter on your slideshow, for the crossing out of objects or for natural looking on-the-fly manually jotted comments.

FORMATTING AN IMAGE

So, now that you have found the images you want, how do you go about incorporating them in your presentation? Here are a few points to consider in making your images look professional.

Aspect ratio: the proportion between the image height and width. Many television screens have distorted aspect ratios as users decide to stretch the image of an old 4:3 movie to a full screen 16:9 aspect ratio. As a result characters appear fat, squares stretch into rectangles, and circles become ovals. To prevent distorting your image, hold the shift key as you click and drag to resize an image.

Resolution: the measure of quality by pixels. Low resolution images look dirty, or pixelated, giving away you are an amateur who unprofessionally copied them off from Google Images. Always use good image resolution, to allow images to appear crisp on a large screen.

Cropping: cutting away bits from image margins. Instead of rescaling an image to fit a specific area on the slide, clip away bits from its sides. Losing a bit of image canvas is a far lesser evil than stretching the picture and risking it becoming distorted in ratio.

Full size: the original image size. There is no reason your image should sit idle and small, adrift somewhere in the middle of the slide. Stretch it out (remember to hold the shift key) without distorting the aspect ratio, to a full page scale. The image should reach the slide edges, and “bleed off the page,” as a print professional would call it.

Here are a few simple steps to create a page-filling image crop. Although you will lose part of the image, the overall composition still looks a lot better than the alternative: stretching the picture and distorting the aspect ratio.

Editing an extension: if the background of an image is relatively even, you can easily extend it to create the right size of an image, without resorting to advanced editing commands in Photoshop.

If you are past 100MB, you file might as well be 100MB

IMAGES AND FILES SIZES

Using images in your presentation can dramatically increase the size of your PowerPoint or Keynote file. Once you are past the 10MB mark, some email servers will bounce back your message. PowerPoint and Keynote both provide options for compressing images, making your presentation lighter.

While compressing does reduce file size, it also reduces the quality/resolution of your images. My recommendation is to keep your images nice and sharp by never going below the 150 dots per inch, for large screens. In an ideal world, you would keep an uncompressed presentation master file on your hard drive, work with it, and compress a copy right before you need to send it off by email.

There are powerful alternatives to emailing, allowing the sharing of large files. My personal favorite is Dropbox. As a side feature of a much larger overall offering, Dropbox allows you to synchronize data across multiple computers and devices, and large files can easily be shared. Instead of emailing the file itself, you email a Dropbox link for downloading the file. There is virtually no cap on file sizes, so, in theory, you can even email an HD movie to anyone this way. You can also share files with someone without the option of downloading the files or accessing them at a later time.

FILE MANAGEMENT

As you start using more and more images in your presentation, your image library will grow. When you save images, it’s good practice to follow some rules that will make it as easy for you manage your images.

Save them in one easily accessible directory on your hard drive. Sync them to Dropbox to make them accessible from multiple machines, if necessary.

Apply a powerful descriptive name to each file, instead of the serial number applied by stock photo sites. This allows you to search for images using keywords. Most stock image files contain pre-filled keywords that can be read by professional image managing programs, such as Apple Aperture. However for smaller libraries, a descriptive file name works well too.

Think about your image purchase as an investment on the future. Often, stock photographers offer different versions of the same image. Maybe one image is cropped a little differently, or the image may have some color filters applied to it. I always try to buy the most basic option possible, with no color effects or cropping, allowing myself the freedom to apply the specific effects and crops I will need. I could then reuse the image for any future presentation, cropping it again in any way I choose.

FINDING LOGOS

Logos work really great for creating attractive slide layout, and work better than entering the company name as text. To get the best possible logo image, you need to observe a number of steps.

Visit the actual website of the company whose logo you need. Companies often change logos, and you’ll want to use the most recent one.

Search for the logo in Google Images, setting the search criteria by size, for medium-sized or large files only. Even if you need the logo on a really small scale, it is always good practice to use high resolution. Large source files render you the cleanest and sharpest images.

Copy the logo file onto the slide, and resize it, holding down shift key to avoid distorting its aspect ratio. Next, compress the image to reduce the overall presentation file size.

Leveraging white space with an image

PUTTING TEXT ON AN IMAGE

Images are often used as a background for text. The best images to use in presentations are those rich in empty spaces, or with a coherent background area, such as a blue sky, empty wall, or grassy field. Not realizing the importance empty spaces play in presentations, stock images often crop images before uploading them for sale. Notice that while the image composition might seem more interesting, the actual file is less useful for you, as a slideshow designer.

When looking for visuals in stock image sites, always scan for images with lots of white space. Some stock image sites let you specify the part of an image on which you may want to add text, and require it to be left blank. If that is not possible, try extending the background of your image, either in PowerPoint/Keynote, or in Photoshop.

Another useful trick, is to put the text over a semitransparent black box. I used this technique in a number of slideshow examples in this book. Set the transparency level of the box according to the specific image you are using. If it is very busy, the box needs to almost be completely black, and if it is reasonably calm, you’ll only need a bit of black.

PowerPoint and Keynote also provide options for drawing a line around text, adding drop shadows to characters, or giving them a slight glow. While all these effects increase the contrast of the text against the image background, I refrain from applying them because the text appears blurry, and somewhat unprofessional. Typographers refer to this effect as “dirty typography.”

Beyond PowerPoint and Keynote

SPECIAL SOFTWARE

Generally, it’s not necessary to use special image editing software for designing presentations. If you do have the budget, try investing in Adobe Photoshop that offers a whole suite of features you’ll find useful as a presentation designer. I won’t go into much detail here, but you can refer to standard Photoshop documentation for help, or turn to the excellent training videos available on Lynda. Here is a brief description of several Photoshop features you’ll work with as a presentation designer.

- Resizing images according to accurate pixel and resolution measurements. This is a better way to control file size and image quality, than the crude PowerPoint or Keynote functionality.

- Sophisticated image manipulation tools for eliminating or extending the image background. Basic proficiency in the software is required. Look for content-aware fill, and content-aware extend.

- The vanishing point filter in Photoshop makes it possible to put text over a 3D object. You can put words or logos on trucks, billboards or walls.

Another interesting application for the graphic adjustment of pics, is Filter Forge, which allows you to apply extreme effects and distortion to images. The application is not cheap, but is very useful. Here are three examples of potential uses for Filter Forge.

- Make all the images in your presentation look consistent by applying the same filter effect. For example, your images can be rendered a cartoon style, or an oil painting look. Filter Forge filters work much better than the PowerPoint or Keynote ones, and even better than those applied in Photoshop.

- Duplicate objects from the pic numerous times, to create images containing replicated instances of one single form.

- Apply a wear and tear effect to an image, giving it a worn out look.

REALISTIC PHOTO COMPOSITIONS

Geared with all the best available software tools, creating well adjusted photo compositions is a challenge even for the most expert graphic designer. Have a look at the blog Photoshop

Disasters for some design failure examples.

For a good presentation, it all boils down to having two choices. You can either create a 100% perfect photo composition, or do not use one at all. Because even if you are successful with some simple graphic editing tasks, such as adding logos or entering text over 3D surfaces using Photoshop vanishing point filter, or even inserting isolated objects with a cropped background, your picture will tarry even from a slight uneven light gradient or color difference. It will look artificial and your whole presentation will become unprofessional. It is better to completely refrain from adding pictures if they are not well adjusted graphically.

Ideally, your images have a consistent style throughout your presentation

VISUAL CONSISTENCY

Good presentations use imagery that is consistent across all slides. It’s often quite difficult to get consistency completely right, but if you stick to a common theme, you’ll have all your images focused around the same visual language. This can be attained using black and white photos, pictures that reflect a certain historical period, or set of unique handmade drawings. Series type of imagery is often also suggested by stock image sites.

Another approach to making your slides visually coherent, is using visual analogies based around a single theme. Introducing a new visual analogy on each slide will tier your audience, especially if the visual language is not uniform. Select a good solid theme for your presentation, considering the most important visual analogy you’ll need. Then apply that theme to all other slides, addressing each concept visually according to this one theme you selected.

QUICK SUM UP

There are many different sources of images available for you to chose from, each entailing different copyright requirements. The key guidelines for a great presentation is to use real, true-to-life imagery, in high resolution with undistorted aspect ratio. Graphically manipulating images are a good solution, but you must make sure the outcome is professional, or you’re better off without.

4 - Layout

Slide layout basics

4 - Layout

Slide layout basics

Slick graphics are not always good graphics

THE TEMPLATE

“Do you have a good PowerPoint template?” I’m asked, or “Can you design a really slick presentation template for me?” I guess people place too much weight on templates, hoping a good one can instantly upgrade the look and feel of their presentation. Unfortunately, it’s not that simple. Most times, slick design does not equal good design.

Perhaps because blank pages with bullet points appear somewhat bare, PowerPoint templates have been relied on to spice things up. This has resulted is all those classical PowerPoint templates we know, full of graphical elements that are repeated on every page of the presentation.

- A wide horizontal background bar for the slide title, and another one at the bottom, preferably with sophisticated textures, reflections, and gradient fills.

- A (big) corporate logo prominently featured on every slide, sometimes featured as a “subtle” watermark on every slide

- Copyright, confidentiality statements and other legal markings.

- Before you even began your design process of the actual presentation content, such elements have already consumed valuable real-estate space in each of your slides. Your slide look cluttered, even before you put anything on them.

My advice is not to refrain from bareness, because a blank page, whether light or dark, constitutes the preferred template. With this as your canvas, use corporate colors to reflect the organization’s graphic style. If you stick to your corporate colors, slides will be highly recognizable without the repetitive use of explicit text or logos, which only bulk a slide.

Include legal statements? If the legal department insists on including copyright text on every slide, try to settle the matter by creating two versions of the presentation, one for live screening on a projector, without footnotes, and one intended for emailing and printing, with the legal disclaimers on every page. If that fails, opt for small fonts and low-contrast colors (such as light grey on white).

Dark for large audiences, light for small ones

Light or dark background? It depends. You’ll find the white background color more practical to work with. It’s easier to make images look good over white, printing is also simplified, as is applying to different formats, such as reading over a PC screen, presenting on a projector, displaying on a tablet. Black background works better for large keynote presentations, where a huge bright white screen on stage can overpower the (relatively tiny) presenter standing next to it.

Forced to use a corporate pre-styled color template? Try these different strategies to allow your professional styling to be used instead.

- Convince your boss (or the corporate communications department) that this presentation is a serious one, viewed by over 4,000 conference attendees. Therefore, a TED-like look is imperative.

- Use as many page-filling images as you can. These cover up the pre-styled logos and standard titles that came with the template.

- Design slides in shades of grey and black, using corporate only colors as accent tones.

Program the correct default values in your template

A TEMPLATE FOR ALL

Artistically designing a template is only half the work of a good template designer. Once the art is set, a template also requires ample programming to ensure it serves even the most inexperienced user. Here are some of the things you’ll need to get right. This programming exercise is likely to have a bigger impact on the consistent look and feel of slides in a big organization than the artistic design of the template.

- The correct default values: Make sure the new colors you define are integrated into the design. Otherwise, the default Microsoft Office color palette will pop up, allowing a different choice of filling for shapes. Properly define the characteristics of shapes and fonts, to ensure the right format will always be applied to the ones added on.

- Delete unnecessary Microsoft template slides: in the PowerPoint slide master view, leave in only the essential four to five slide templates, including a title page, separator slide and a blank one. Microsoft includes many others by default. If you taken them out, nobody will be able to use them (by accident).

- Add example slides: ship the template with a number of example slides that are based on the template that you have designed. Example slides can include a large picture slide, a column data chart, a contents page, a separator slide, a data table, just to name a few.

- No bullet points in the default new slide: delete the list of bullets in the first slide. Bullet points should not appear as the standard inline text style.

I have seen many examples where corporations hurriedly skipped these technical adjustments required for making a deck of slides look good. Before releasing a template to the entire organization, it is very much worth the wait, as critical elements of a solid template are ironed-out. It will be difficult to fix things once the genie is let out of the bottle.

LAYOUT BASICS

There are a few things you need to pay attention to when designing a good layout for your slides.

Grid: graphic designers use a mental grid for placing elements in composition over a page. Every element is aligned with another. While the actual grid is not visible to the reader, and elements seem to be positioned effortlessly, it is this grid that governs a good look.

Although presentation layouts are different from seven-column newspaper layouts, it does pay off to take the grid into account when designing your slides. Never place an object randomly on a slide. Always align objects, and always redistribute them when you make a change. Apple’s Keynote is especially helpful in this. As you drag an object across the screen, yellow lines appear to suggest new preferable locations, either to the left, right, or center of another object, or distributed evenly between a series of objects.

Some elements of a slide have a visible grid, for example, tables, feature tradeoff lists or pro’s and con’s, head shots in management team overviews, client logo pages, or project timelines. Recognize the grid, and position things according to it for a nicely tailored page.

Do not give your audience a reason to wander off

Align and distribute: minute imprecisions in alignment make your presentation look unprofessional, and will bite into your audience’s attention. They’ll be thinking “Why aren’t all these boxes snug on a straight line?” It’s like a crease on a straight curtain, a picture hung crocked on the wall. “Shall I get up and fix it, or leave it as it is?” Wondering about such details, prompted by your slides, and audiences become oblivious to what you are saying. So, eliminate any excuses for distraction by always aligning and distributing things properly.

Avoid symmetry: invitations to children’s birthday parties and odd ads posted around the company’s water cooler, are often centered across the page. This symmetric composition is not one most pleasing to the eye. Use the Golden Ratio (Golden Section) proportioned by classical painters and architects. It is 1:1.68, indicating the best way to divide a slide is roughly two-thirds down the page.

Have a look at paintings, inspect advertising billboards. You’ll find designers put things off centre. Many camera viewfinders display a nine box grid over three vertical and horizontal lines, to help you frame a picture. You can apply this supporting aesthetic logic to your slide design as well.

Eye movement: a complete slide is absorbed in our brains in stages, not simultaneously. The most prominent item is taken in first, then the one after that, until all details are registered together as a whole. Good designers predict audience eye movement across all slide items, and consider this in their design.

Think about the line of vision you want your audience to follow when your slide is shown to them. Recreate it as you design your slide, incorporating such visual preferences to ease-in the absorption of a slide as a whole.

To loudly attract attention, you can decide to stage a screaming contest, bolding out important elements, flaring them with color and size. Yet, if you overdo it, the slide will appear way too busy for any audience to capture its message in its entirety. A subtler approach is often more effective.

To show relationships between elements, you can use direct indicators, such as a connecting line or arrows between objects. Yet, an indirect approach can be equally powerful, for example, applying the same color or shape to a set of items immediately hints at their relativity without the use of arrows or connecting lines. You get the relationship across in a much cleaner look.

There are secondary traits that also play a key role. For example, in the West, good things are implied from left to right, and bottom to top (we do all love those sales and profit forecasts that reach up to the sky.) Make sure elements on your slides follow this direction (unless, of course, you want to present a heavy downturn in your business.)

Spectacular effects usually do not help your story

Easy on the animations: PowerPoint and Keynote can produce spectacular animations, but these must be used wisely, if at all. Just because a software offers a tool, it is not necessarily beneficial to all cases or at all times.

Flying objects, wild zooming effects or spinning headlines, more often than not distract your audience’s attention who stray to wonder what else is going to pop up next. Even worse, effects may raise giggles, setting the room off on a less attentive mood, and your story will lose relevance. Avoid this in a serious pitch presentation, for potential clients or investors.

Another problem with animations is a technical one, considering they do not render well in formats such as PDF, tablet, or webinar presentations. If you are inclined to use these formats, refrain from adding animation in your slide design.

Animated slides are also very hard to edit. Selecting objects becomes really though, and it is even harder to get the sequencing of everything right. (Tip: if you use PowerPoint 2010 for Windows, look for the Selection Pane on the Help menu, to make your life easier with editing multi-layered slides.)

With all things said against slide animation, it can prove useful in some cases. For example, a complex structure, such as IT system architecture, is best explained gradually by introducing elements in an animated process, guiding the audience’s line of sight. Here, the sequenced pop ups of animation serve a clear purpose and are beneficial. In contrast, it is not good practice to use animation for exposing a ten line paragraph, revealing it bullet by bullet.

You can recreate pop up animation without using the actual animation function in PowerPoint or Keynote. Do this by creating a series of almost identical slides in sequence. Each slide adds more detail to the previous one. In PowerPoint’s Slide Sorter view (Light Table view in Keynote), you will see different slides, but the audience perceive them all as a single one. Start by designing the final completed slide, with all its complexity, duplicate it a number of times and take out bits as you go back in time.

The added benefit of this approach to animations is that you can change slide headline with each additional iteration of the build-up.

Frameworks are visual buzzwords

FRAMEWORKS

Business bestsellers and consulting documentation are filled with sophisticated, fancy frameworks that boast an even fancier name (7-S, Porter box, SWOT, etc.) These are often designed for a very specific need, and applying them elsewhere can hardly work well at all. It’s much like trying to make your presentation look important by adorning it with industry buzz words.

I am a firm believer in very simple diagrams, showing only the required information, compiled separately for each situation. And most of the time, the simplest diagrams are the best ones.

An overlap, combining “best of both worlds,” a Venn diagram with two overlapping semitransparent circles (or rectangles) where the overlapping field shows up darker in color.

A table with an options axis and an evaluation criteria axis. You can add color and use plus and minus (+-) signs to create a favorable comparison of how you stack up better against competition, and why yours is the preferred option. If the two or more rows address similar issues, consider collapsing them into one row with a slightly more generic title.

A 2x2 or 3x3 matrix that maps options, markets, or competitors on a two axes grid. Position yourself in the top right box, of course, all on your own. Note that if you cannot fill the bottom left box in a 2x2 diagram, you might as well use a simple Venn diagram to make your point.

THE 10 SECOND TEST

To ultimately test your design layout, flash one of your slides on a screen for roughly 10 seconds, close it and ask a volunteer to play out its key message. If you find they are unable to do this, you’d better give the slide another design iteration.

QUICK SUM UP

The best slide layouts are often simplest ones: a simple template without clutter, organized around a mental grid structure with minimal animations and sophisticated frameworks.

5 - Fonts

What fonts to use in your presentation

5 - Fonts

What fonts to use in your presentation

Fonts greatly impact the look and feel of your presentation. If you are bound by a corporate presentation template, where font use has already been decided for you, skip this section and move on to the next chapter. If not, its important you make a number of educated decisions regarding fonts.

CUSTOM OR STANDARD FONTS

The first choice you have to make, is whether to use custom fonts or stick to the standard ones installed on your computer. When you open a PowerPoint or Keynote file, any custom font not installed, will automatically be replaced by your operating system. While this might work for a textual document or email, it is a disaster for a carefully crafted presentation.

Your characters will look different from what you intended and the worst of it is, that different fonts have slightly different sizes. Text boxes created just wide enough to fit a crucial sentence, now suddenly cut off an extra line added due to the random font replacement. An entire chart can be thrown into chaos.

Such font issues only occur with software that enables text to be edited, such as PowerPoint, Keynote, Word, etc. In other file formats, such as PDF or images (JPG, PNG), fonts are baked in as pixels, so the text appears just as you designed and intended it, regardless of the fonts installed on your machine.

PowerPoint offers the ability to similarly embed fonts into a presentation, but this feature only works on the Microsoft Windows platform. In PowerPoint for Mac OSX, you cannot do this. With an increasing number of people switching to Mac platforms, I would hence not rely on custom fonts.

Tablets and mobile devices create additional issues for fonts. The font library on a mobile device is even more restricted than that installed on a Mac or a Windows machine. Mobile technology has progressed, but in 2012, presenting a full deck of slides on a mobile device is not customary.

People check their emails more and more on the go, and your presentation will suffer if it is not legible on their devices because of poor font choice. Create a presentation that will look good on any station or device.

Usually, sans serif fonts work better

STANDARD FONTS

There are two basic types of fonts, serif and sans serif. Serif fonts have little extended hooks at the bottom of each character, and sans serif do not.

For printed copy, serif fonts work great because these hooks help the eye connect between letters on the page you hold. It is similar to cursive handwriting in that sense, and makes it easier to read the text, especially in small font sizes. For on-screen presentations, sans serif fonts are the better option, since they come across clearer in larger font size. In print, designers often use several fonts. Body text is set in one font type, headlines in another, page numbers and footnotes in a third.

For presentation design, it is best to stick with one font to gain a calmer design. If you think about it, all text in a well designed presentation is actually a heading.

GOOD STANDARD SANS SERIF FONTS

Windows: Calibri is standard serif font for PowerPoint. It’s an attractive typeface that’s very legible, but it has fallen victim to its own success, popularity over-identifying it with PowerPoint. You cannot use Calibri and expect to create a “PowerPoint that does not look like PowerPoint.” On a Windows machine, I prefer Arial, the Microsoft variant of Mac’s Helvetica. Arial Black in all-caps looks surprisingly well.

Mac: unlike Microsoft, Apple did decide to pay royalty fees for Helvetica and it’s installed as a standard font on all Apple computers. Helvetica is an excellent choice for a presentation font. Windows automatically replaces Helvetica to Arial. Apple itself uses the font Myriad Pro in its presentations. It looks good, but they run the risk of font replacement, since it is not installed on Windows computers.

iPad: the latest version of iOS includes a fairly rich set of fonts. You can check the web site iosfonts.com for a complete list. If you are working within the Apple ecosystem, pick your standard font from this list to ensure your presentation can show up nicely on both Mac and mobile device.

No Comic Sans please

A FONT TO AVOID

Comic Sans has been profusely used in children’s party invitations and secondhand car ads. Your presentation will inevitably resemble these too if you chose to use this font.

OTHER STANDARD FONTS

Its worth considering these fonts for your presentation, but remember to first check if you like their appearance on mobile devices.

- Century Gothic, a light and elegant font.

- Franklin Gothic, includes a good narrow variety.

- Verdana, very clear for screens, but is very wide and less efficient.

If you cannot decide on a font, use wordmark.it to display a string of text styled in the variety of fonts installed on your computer.

CUSTOM FONTS

If you decided to go for custom fonts, you have the entire universe of font possibilities at your disposal. Still, its advisable to exercise restraint. Custom fonts I use most frequently include different weights of Helvetica, with medium for body text, and bold condensed weight for headlines.

With Arial, the problem is not so much its shape being somewhat less elegant than Helvetica. It’s the fact that it only comes in very limited weights, regular and bold, and correctly choosing the weight of a font has the biggest affect on the visual appearance of your text.

For a more industrial look for your presentation, try setting headlines in the all-caps Beebas Neue, a free open source font, or League Gothic for a narrower setting.

You cannot go wrong with these classics

FONTS CONSIDERED CLASSIC

This last century has introduced a number of fonts considered classics by professional print designers. Here is a partial list that will look good in a presentation design.

- Helvetica Neue, and Helvetica Neue Condensed.

- Frutiger, a predecessor of Helvetica, designed for airport signage.

- Futura, going back to the Bauhaus movement, also look at the Condensed Extra Bold variety which I use for the Idea Transplant logo. Futura is great mainly in all-caps.

- Gill Sans, the original font of the London underground.

- Meta, very legible on screens.

- Myriad Pro, the corporate font of Apple, applied in all their communication.

- Optima, somewhere in between a serif and a sans serif, very elegant yet less legible on screens.

- Univers, a classic similar to Helvetica, which also comes in endless amounts of weights.

There are many books about fonts and typography. The mother of all such books is the Font Book, weighing some 3kg. Luckily, an iPad version has become available. Weighs a lot less and affordable a lot more.

And now for something completely different

OUTRAGEOUS FONTS

Sometimes a slide design may require an outrageous font, for extremely funny text, extra loud messages, fat styles, handwritten notes or cartoonish messages for which Comic Sans won’t do.

If you use such a font in one slide only, it’s not worth the effort to require its installation on your viewer’s machine. Instead, create the required text on your own machine, save it as an image, and paste it back in your slide. Remember to copy the original, editable text to an appendix, in case you’ll need to make revisions in the future.

Font Squirrel is a site that offers a rich library of free fonts, and is a good hunting ground for the unusual ones. In book stores you can find numerous print books that come complete with CD-ROMs showcasing free fonts.

Here are some examples of outrageous fonts I had a chance to use in the past.

- Boopee for a handwritten effect that looks a lot better than the profusely used Comic Sans font.

- Impact Label mimics the look of a 1970s labeling machine.

- Feast of flesh is the basic font type of the Angry Birds game.

- Boycott is a grunge, distorted, font that comes only in caps.

- American Typewriter used in the famous “I heart NY” logo, it is another option to consider.

FONT SIZE

There are no rules for the right size font, only general guidelines. A font smaller than 18 points will prove hard to read for audience sitting in the back of the room. I always use PowerPoint’s Slide Sorter view, or the Keynote Light Table view, to present a series of slide thumbnails in front of me. This gives me an idea of how legible my slides are at a distance.

Having said that, bigger size font is not always better. If your slides have ample free space, it might be better to keep it blank. Maintain an elegant, moderately sized text line, instead of filling up the page with large typography.

Software is optimized for using text intended for reading, at 12 - 18 points. Using fonts bigger than these entails increasing the spacing between lines, the so called leading. By default in both PowerPoint and Keynote, the leading between two lines of text is set to 1.0. This means that if you use font size 14, your text leading will be 1.0x14 = 14, as well. This works fine for smaller font sizes. For larger font sizes, I recommend going down to 0.8, or 0.7.

Emphasizing by de-emphasizing

HIGHLIGHTING TEXT

The intuitive approach to highlighting text for emphasis, is applying the full artillery of typographical tools: bold, italic, ALL-CAPS, or ALL OF THE ABOVE. I find the result is unattractive, and will give your audience the impression you’re broadcasting your message too strongly.

Instead of highlighting text, design your slide so that the text naturally stands out. For example, de-emphasize its surroundings, use white space or color differentiation between text items. A subtle use of bold can look good on a slide, but underlining never does.

QUICK SUM UP

Keep your font choices safe, to ensure your presentation looks great on as many devices as possible.

6 - Data

Data visualization in presentations

6 - Data

Data visualization in presentations

Quantitative facts and data can be very powerful for supporting your message, but they may cause confusion if not presented legibly on a slide.

Picturing data is hard

Why does it go wrong so often, when numbers and quantities are displayed visually?

- It is very hard to pick the right numbers to present from a defined set of data, usually drowning us with overload. Which should I show? The absolute values, % of the total, % growth, margin %? Huh?

- There are so many data charts to choose from, pie, column, line chart. Which is the best?

- The standard data templates in PowerPoint, Excel, and Keynote appear cluttered. How do I make data look clean and clear?

One message per chart, especially in data charts

The “so what?” angle to data

Let’s start with the first issue, and get in grips with how to survive in the overflowing data world. My basic training as a consultant at McKinsey taught me a useful concept called the “so what?” of a chart. This pinpoints the essential one fundamental message of a data chart, so all other facts, figures or graphs should serve this purpose alone. In your presentation, clarify this point to yourself, and support this one key concept only, nothing else.

So, before designing your chart, you must pinpoint what it is you want to say. For example, our sales in the US are growing in dollar terms, US sales are becoming increasingly important in our portfolio, growth rates in the US are slowing down, a drop in volume is offset by an increase in prices. While the same data set can answer all of these, and each requires a completely different type of chart for its visualization. Decide on the most important trend that you want to show. Once you have defined it, picking the right data chart type is easy.

Which chart?

Of the many different types of charts available in Excel or PowerPoint, I tend to use only a few. Here is my short list.

- Column chart: good for indicating progression over time, in sales or profits and users visualization.

- Bar chart: used for ranking, the largest players in an industry or the lowest cost producer. Make sure you sort your bars in ascending or descending order, to add an additional visual clue about the relative position of a number in a series.

- Stacked column chart: good for depicting market shares, or components of a whole. I like these better than pie charts.

- Line chart: used for displaying a trend made up of many data points, for example, world population since 1850, and for visualizing multiple trends together on one chart. Make the line of such charts really thin, to let it stand out on the screen.

3D charts are harder to read than 2D ones

Manual design in 2D

The standard data chart templates in PowerPoint and Keynote are ugly and cluttered. Here are some fixes you can do to make them look cleaner.

- Remove tick marks and grid lines and make the axes thicker.

- Remove the automatically generated legends, and make your own instead. Use larger boxes better positioned on the slide as an entirety.

- Remove and create your own slide titles, positioning them manually on your slide so they line up with all other elements on it.

- Set spacing between two columns or bars to 50%.

Keynote and PowerPoint offer a wide range of 3D data chart templates. However, 2D designs look much better, and are also easier to read, with bars lining up better neatly next to each other neatly.

Newspapers such as The Economist or the New York Times often use data charts that have a simple, clean style. Try to replicate this in your own presentation.

Data charts in Excel, used for analyzing, slicing, and dicing data, can (and should) be generated automatically. If you are not 100% sure what the key trends are, and you need to quickly draw and change data charts, automated charts are great time savers. Once you are ready to design the presentation, you’d have hopefully passed this stage. To present your conclusions, spare the audience the effort of going through the data analysis process. You’ve done the hard work and can feed them the answer directly. To do this well, you must carefully design data charts manually, answering to your “so what?” definition. A quick cut and paste from Excel will not do your presentation justice.

Round up numbers to make them clearer and appear more credible. $52.3M is easily grasped in comparison with the full $52,345,548 number. This also makes the presentation look solid. While it’s important your Excel model calculates everything with full precision, only to hand you complete, long numbers, your audience probably won’t buy into your exact prediction of year 5 sales yielding $52,345,548, precisely. So, save everyone the trouble and round up your numbers.

You can take this to another extreme, by applying ranges using only the mean number, for example, 7 for a 5-10 range. This could work, for one single data point, but once additional variables are involved, you’ll need to include them in your calculations too, making everything very confusing. Instead, offer a big caveat upfront, and continue to work with your point estimates throughout the presentation.

Charts are only the beginning

Even the most minimalist data charts can be hard to grasp by audiences. To simplify things, add text boxes, arrows, lines, circles, and apply all the drawing tools available to accentuate your point. A big arrow across columns can readily indicate growth, a circle around the turnaround in gross margin will emphasize it, etc.

It’s not a chart you’re designing, but the slide as a whole. Where more than one graph appears on a page, align and distribute them properly, with all the horizontal axes lining up. Draw a temporary line across them to double-check, and make all the charts roughly the same height. Take notice of titles and other objects’ positioning and alignment on the slide.

Looking good

Yes, it is wrong to lie with statistics. I refrain from breaking axes or using other tricks to stage a modest growth as a huge jump in sales. On the other hand, poor design can damage your case. For example, if you only have two years of sales data to show in a column chart, stretching it across a 16:9 screen will flatten sales trends. Instead, shrink the chart until it fits well right in the center of the screen.

Putting things in perspective

Sometimes numbers are so small, or so big, that audiences are virtually unable to grasp them. A slide stating the world’s population of 7 billion is meaningless to people. You need to conjure up a quantitative metaphor that tangibly compares your values. For example, liken the emptiness in an atom to the space around a strawberry located in the middle of a football field, its electrons flying round on the podium seats. If you add such a metaphor in text, or, better yet, accompany your slide with a picture of an empty stadium and a tiny red dot in the middle, the information is sure to resonate well with your viewers.

Not all data charts have to be simple, containing only several figures. To convey a message that numerous instances exist for something, you can show a world map covered with dots.

Props

The message of a chart must always be easy to grasp, but may require complex charts that weigh it down. Instead, consider using props, such as real live pictures. Where possible, bring the real thing in and demonstrate it on stage with you. In a presentation I recently attended, a picture was shown with several empty bottles of soft drink above a bag with the corresponding amount of sugar they contain. It served as a very convincing data visualization prop.

Every analysis is always accompanied with extra information, unit measurements, footnotes, data sources. Ultimately, all this information should fit on the slide, somewhere. This is especially true where you’ll want to reproduce analysis of an older deck version, or drill-down into its substance. Keep in mind that this information serves best as secondary input. You do not want to overdose your audience with too much clutter as they first see the chart. Place such data in small font or soft colors, to hint they are less pertinent to the chart, and are optional for reading. You’ll find most of your audience will skip them.

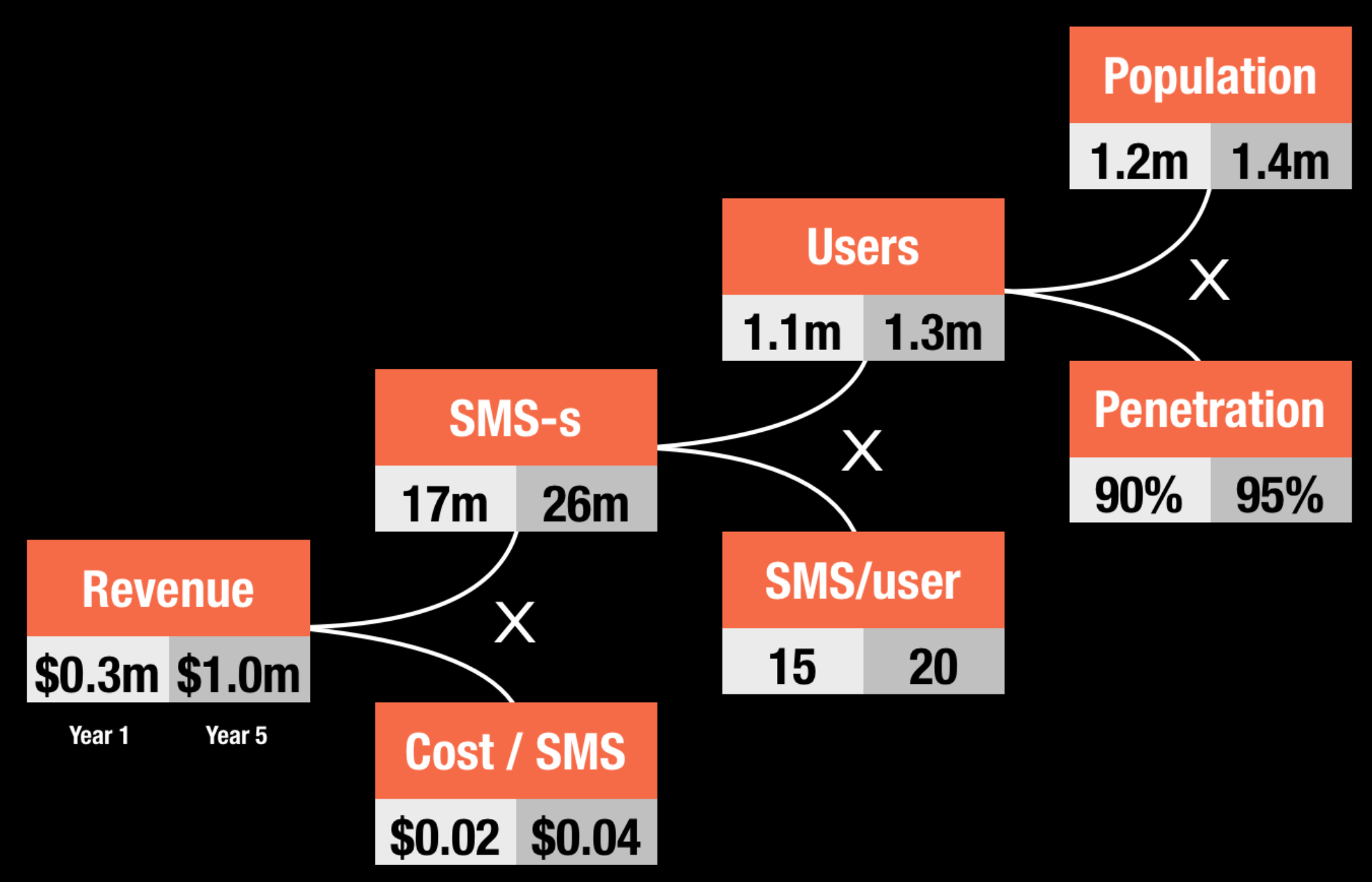

Sometimes, a simple data table is best

Data tables

Sometimes, you do not need a data chart at all, and a handsome table containing rounded numbers might just be the right option with which to visualize your data. This works great for detailed financial statements, or in situations where a chart contains numbers with completely different orders of magnitude.

Here are some quick improvements you can make to any table (Image 6.2):

- Space out rows and columns, the more they are the same size, the calmer the look.

- Round up numbers to a reasonable precision level, and use a comma to separate numerals.

- Right-align numbers, and make sure they are aligned on the decimal point.

- Right-align the first column with its descriptive text, so that it’s as close as possible to the first column with numbers.

- Use highly muted backgrounds. I usually pick the lightest shade of grey, and color the cell borders white.

- If necessary, reduce font size. Very big fonts with unnatural line breaks do not look good in a table.

- Enter data manually. Meticulously typing in every number is often the only way to give your table the look you want. Invest the time and do this. It’ll prove well spent.

As you work on visualizing data, remember that people get used to interpreting info in a specific way. Think twice before you dramatically reinvent methods for visualized numbers in your presentation. A company’s Board of Directors, for example, has become accustomed to seeing quarterly results from dozens of previous quarterly presentation. These have trained the Board Members to think about data in a certain way, which is hard to change.

Some presentations leave you with no other option but using a dense data table. For example, quarterly results presentations require the accounting data to be presented without rounding off errors. In such cases, add the table of raw data to the deck, but use a selective data chart to highlight apparent trends.

Where is the meat?

It is tempting to cut the amount of data in your presentation and simplify your story, but an important distinction between evidence and detail must be maintained. While detail can be cut, crucial evidence must remain intact. Go ahead and replace a slide that ranks market shares with the single textual sentence “We are the largest in our industry.” Yet, presenting the actual data, or naming your (much smaller) competitors, can prove much more powerful. This is especially helpful to people that hear your story for the first time.

Waterfall charts

I often find data I present does not reflect what’s really going on. You may need to go back to your analytical drawing board, recut numbers, and bring trends to life in your presentation.

A favorite analysis presentation tool I learned back at McKinsey is the Waterfall chart, also called the Source of Change chart. This is a stacked column chart in disguise, explaining how values are bridged (for example, this and last year’s profit) using a number of drivers that follow the same or opposite direction.

The most difficult aspect of the waterfall analysis, is calculating the actual numbers. Once you have figured those out, it is relatively easy to place them in PowerPoint.

Data charts should be helpful

Data visualization can sometimes be taken too far. Today, the infographic is a very popular way to visualize data. These are cool, cute, and nice, but a closer look shows they often fail in helping you better understand data. Graphic design is used for cosmetic purposes only. Simple visualizations of one single trend prove to be the clearest.

Quick sum up

Data charts should have one “so what”, and focus the entire chart on that message. Resist the temptation to cut and paste from your spreadsheet, but rather design the chart from scratch, manually if you have to.

7 - Story

Creating a presentation flow and story

7 - Story

Creating a presentation flow and story

The power of stories

Most presentations start with a bulleted agenda page that described what’s expected to unfold.

- I will introduce points 1, 2, 3, and 4

- I will discuss point 1

- I will discuss point 2

- I will discuss point 3

- I will discuss point 4

- I will summarize points 1, 2, 3, and 4

Then, the speaker is likely to take up too much time explaining the first point, and then races through the rest, telling the whole story relatively quickly. At the end, again too much time is invested in redundant repetition of what the audience has just seen and heard. It’s the common, yet uninspiring, strategy of “Tell ‘m what they’re gonna be told, tell it to them, and then retell ‘m what you just told.”

In education, repetition is used to "force" children to learn

Centering on repetition to attain results, is a strategy often used in education systems. Teachers repeat material over and over again, until the brains of their uninterested students are bent to remember some. This memory pattern cannot be relied upon. All is forgotten a day after the exam. Much like factories, many educational institutions also maintain a production line, of diplomas, powered by grades. In the end, most students face no other choice but to cooperate and jump through the hoops.

In presentations, repetitive pounding of facts on the heads of investors or potential customers will eventually shape their brains in your angle, but their minds will remain untouched, making them indifferent to your message, bound to forget it immediately.

Stories are the empowering tools granted humans for effectively conveying messages and information. I imagine any system will prove successful if compulsory compliance was taken out of the equation, and a creative plot forms the central element. (Why, even the young generation will be excited in an education system that invites them to really apply their minds and hearts.)

Stories spark natural curiousity

Telling it so

Instead of a presentation designed to be an endurance test, create it as a story. Your message can best stick if you were to tell it so.

“For sale, baby shoes, never worn.”

This is a famous short story by Ernest Hemingway, the shortest he ever wrote, and his favorite. Our minds are immediately intrigued, asking questions, “Why? What happened to the baby?” and we wrap our own imagination around these words.

Human nature requires an inspiring structure, a motivating framework, with which to relate to things and remember them by.

You’d have experienced this, brainstorming ideas in a team in front of a whiteboard. After an hour of discussion, it’s covered with scribbles reflecting the heat of the debate. If you snap a picture of the whiteboard on your mobile, there’s a good chance it’ll remind you of the entire session, word-for-word, even weeks later. It’s not the quality of the notes on the whiteboard that trigger the memory. In fact, these could be completely illegible. It’s your brain connecting pieces of the session (hi)story with physical elements on the whiteboard. 3D spatial structures help recall the full richness of the debate.

Bulleted lists only hint at the story

The human brain was not designed to remember bullet point lists, or the telephone numbers of an address book. Rather, our ancestors had to rely heavily on spatial memory to recall locations for finding food. Then, after eating those apples from the tree, they had to remember their way back home, carrying ripe fruit for their family.

Another example for this notion, is a trick used for remembering a random series of objects. Imagine the objects along a familiar route, such as your commute to the office in the mornings, where the elephant is next to the train station, ducks are under the viaduct, and a bike is in front of the windmill. Creating a simple visual storyline in your head, literally seeing the objects upon the familiar route, is a simple way to memorize a list of objects. If you are interested in reading more about how our memory functions, I recommend the book Moon walking with Einstein by Joshua Foer.

So, in presentations, your story constitutes the (emotional) framework over which your audience can store the information in their brains.

Business presentations are stories as well

Some argue that a business presentation can never be as exciting as a movie or a novel. While this may be true to most, it is perfectly possible, and highly recommended, to apply story telling in business contexts. You’ll find that corporate minds relish inspiring and motivating plots.

Take a customer case example for instance. Most case examples in business presentations consist of wordy customer quotes, full of fuzzy language. “Company X really gave a best-in-class service to provide my company with a scalable and flexible architecture solution.” Uhu...Okay... And?

Instead, tell it so that its more experiential, with the essence placed on the plot: state the customer’s problem and explain how you solved it, wrapping everything up with enriching and entertaining anecdotes that will allure your audience.

Here’s another example. One way to describe the customer’s problem solved by your product, is a simple bulleted list. Another way, is to describe a day in the life of a customer, from getting up in the morning to bedtime at night, highlighting examples along this timeline, where other market solutions fell short and your products helped.

You can introduce your presentation using an actual story, and provide and anecdote in the end to accentuate the story as the underlining message about your company. Throughout the presentation you can come back to the story, with analogies, as you introduce more concepts and give more information.